The Analysis Is Better. The Opportunity Is Worse. How to Decide in an Emerging Market

The investment committee asks for one more study. Not because the project is weak, but because the numbers aren't "settled."

Six months later, the analysis is better, but the opportunity is worse. Policy has shifted. Feedstock prices have moved. Customers paused their commitments. In the energy transition, this isn't an exception; it is the norm.

Whether it’s SAF, hydrogen, or CCUS, we are building in markets that are still forming. Which means the real question is rarely “do we have enough data?” It is: How do we decide when the data will never be complete?

Why Transition Data Doesn't Converge

In conventional infrastructure, you analyze existing markets. In the energy transition, you create them.

Technology economics are revealed by deployment, not spreadsheets.

Policy is negotiated. Mandates and tax credits evolve in response to real supply.

Liquidity follows participation. Bankability emerges only because early projects establish the reference points.

Much of the data investment committees crave simply does not exist ex-ante.

A Framework for Decisive Governance

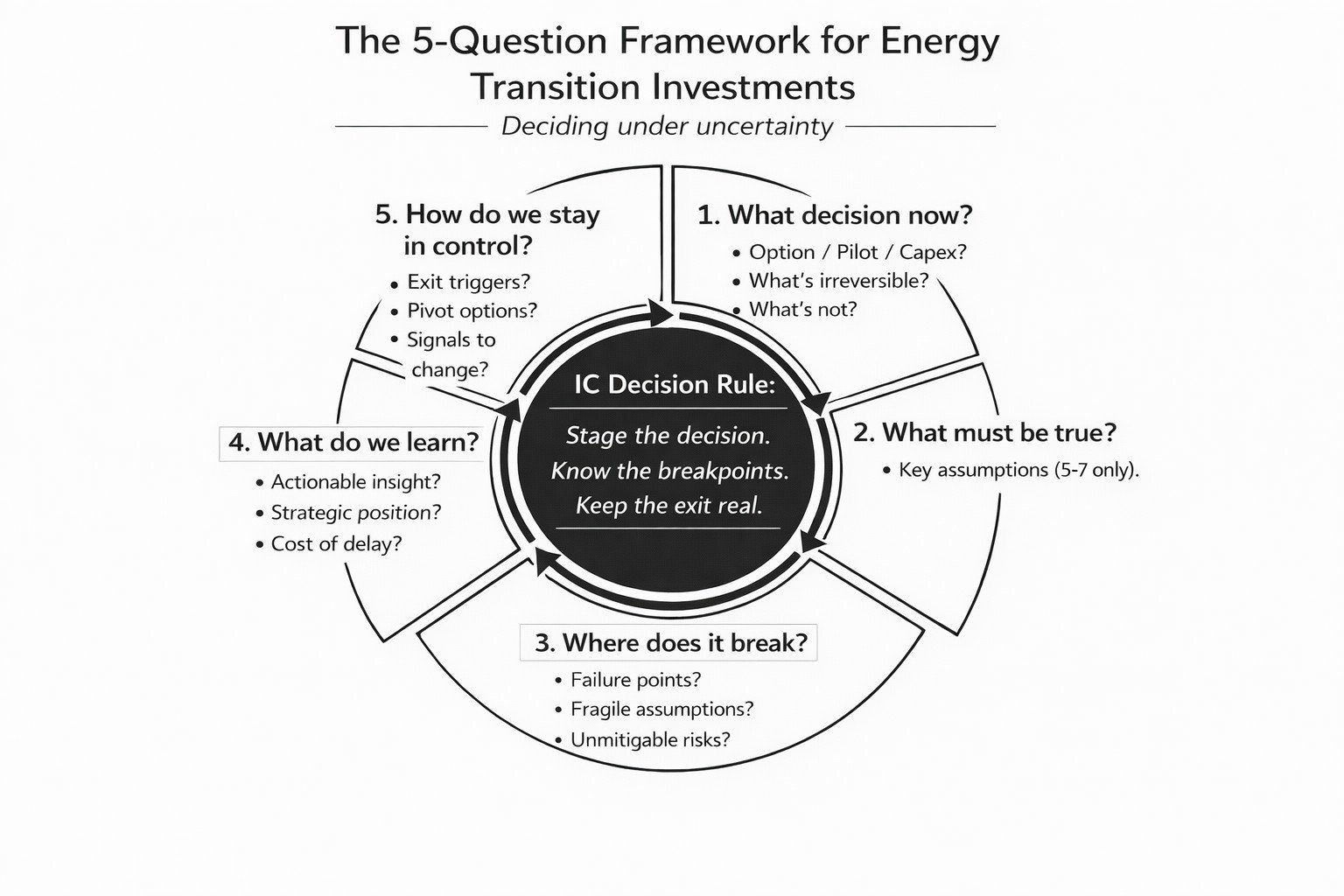

Strong committees don’t rely on more complex models. They rely on five disciplined questions.

1. What decision are we actually making now? Precision matters. Are we committing total construction CAPEX, or just funding FEED and securing feedstock options? Most committees collapse multiple gates into one, inflating perceived risk. What becomes irreversible after this vote, and what does not?

2. What must be true? Uncertainty is broad, but success usually hinges on a few variables: policy eligibility, feedstock cost bands, and offtake beyond compliance volumes. If everything matters, nothing is being managed.

3. Where does this break? We spend too much time optimizing base cases and too little time identifying failure points. If feedstock spikes by 30% or mandates soften, does the project survive? A project you do not know how to kill is a project you do not understand.

4. What is the cost of delay? Waiting feels prudent, but it is a strategic choice. First movers shape the standards. Policy frameworks often crystallize around operating plants, not proposed ones. What do we lose by letting others take the learning risk?

5. How do we stay in control if we’re wrong? Decisive investing is about retaining control when assumptions fail. Before committing capital, insist on:

Explicit pause/exit triggers.

Observable signposts (policy shifts, offtake milestones).

Modular designs and staged capital.

A worked example: SAF production

Consider a proposed SAF facility targeting a regional aviation hub.

Key uncertainties include feedstock pricing, long-term offtake appetite, evolving mandates, and certification treatment. No amount of upfront analysis will fully resolve these.

Using the framework:

Decision now: approve front-end engineering, feedstock options, and conditional offtake negotiations—not full FID.

Must be true: minimum anchor offtake beyond compliance demand; feedstock secured within a defined cost band.

Breakpoints: failure to secure anchor offtake within 12–18 months; adverse policy change affecting eligibility.

Learning: real data on feedstock logistics, yields, airline contracting behaviour.

Control: staged capex, modular expansion, pre-defined exit if triggers are hit.

This is not betting the project. It is buying structured learning while keeping exits real.

The Bottom Line

When data is imperfect (and in SAF it always is) stop asking if the analysis is complete. Instead, follow a simpler rule: Stage the decision. Know the breakpoints. Keep the exit real.

Energy transition leadership isn't about eliminating uncertainty; it’s about deciding which uncertainties are acceptable and which are fatal. Data will never replace judgment.

The question is whether you are prepared to exercise it.